ATTENTION:

first time & repeat home buyers

Why Your Mortgage Strategy

Matters More Than Your Interest Rate

The way you structure your finances could cause you to pay significantly less in interest—without increasing your monthly budget or sacrificing your lifestyle.

CLICK BELOW TO Learn how!

Mortgage Calculator

Your Estimated Results

Notice Something?

There May Be A Better Way

ATTENTION: first time & repeat home buyers

Why Your Mortgage Strategy

Matters WAY More

Than Your Interest Rate

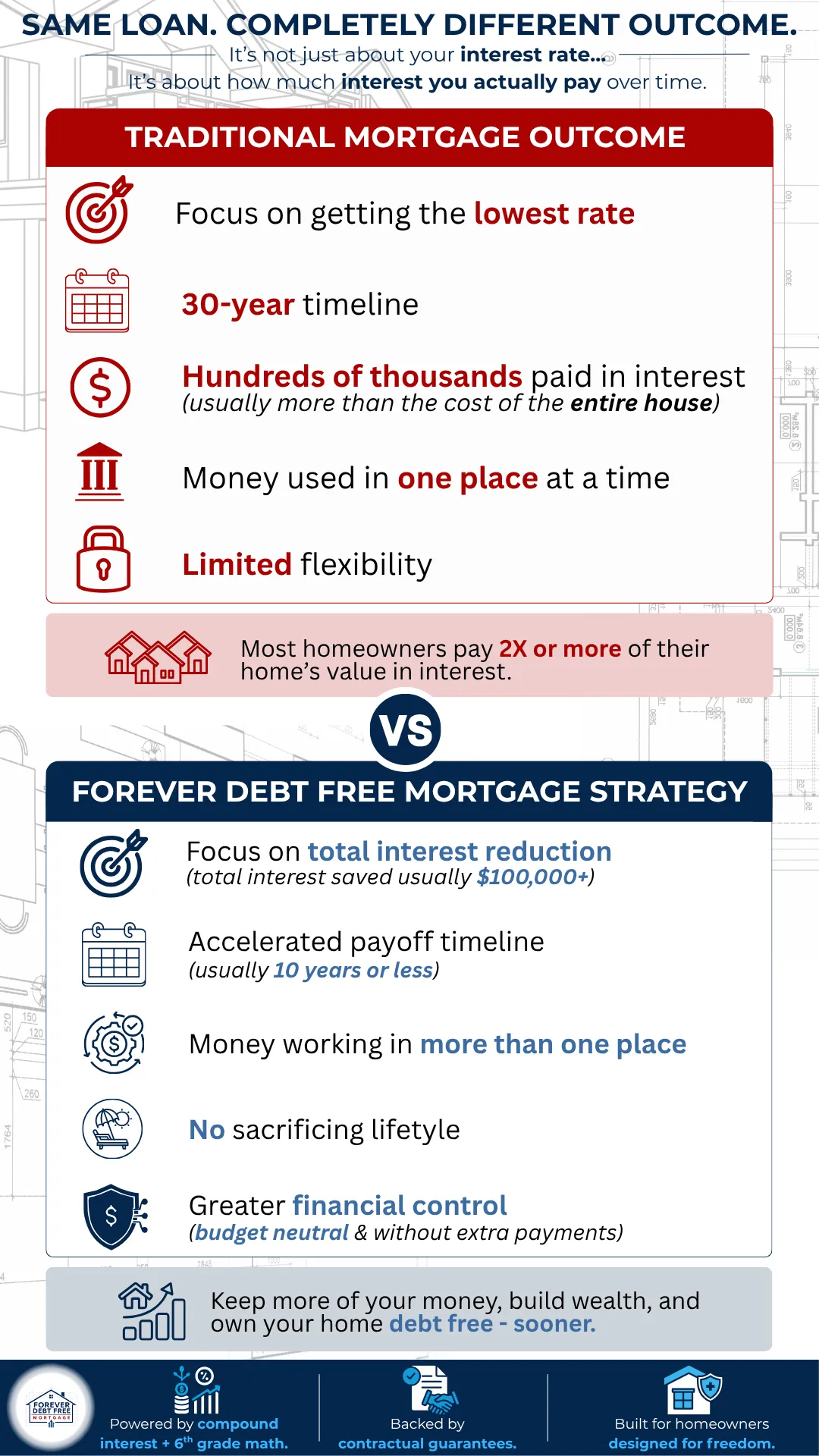

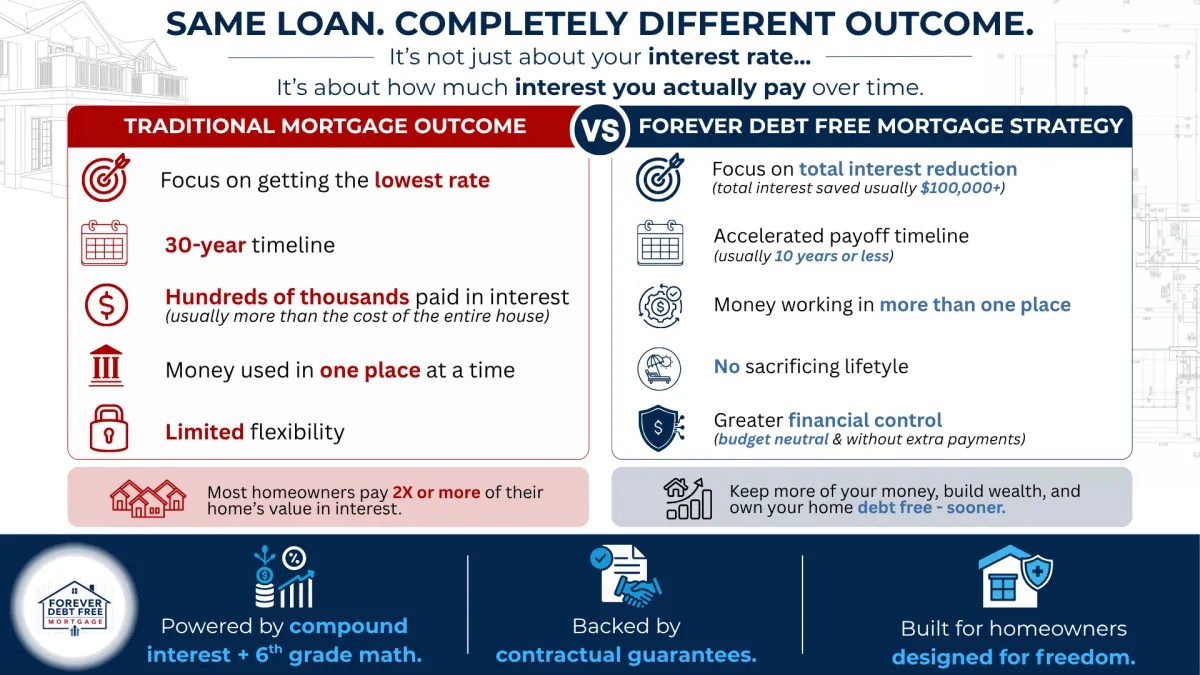

On the average 30 year mortgage, we help qualified clients structure their loan & their cash flow with a strategy designed to have the home paid off in 10 years or less. For most qualified clients, that means saving $100,000+ in interest payments while building $100,000+ in liquid capital - all without increasing their monthly budget or sacrificing their lifestyle.

CLICK BELOW TO Learn how!

Mortgage Calculator

Your Estimated Results

Notice Something?

There May Be A Better Way

You weren't taught this in school, but...

The Traditional Mortgage Path Is More Expensive Than Most People Realize

Going By The Numbers (national averages)

WHAT MOST PEOPLE LOOK AT

Home Price

$400,000

Loan Amount

$350,000

Interest Rate

6.5%

Monthly Payment

~$2,200

WHAT YOU SEE...

WHAT YOU ACTUALLY PAY

WHAT IT ACTUALLY COSTS

Total Paid to Bank

$800,000

Total Interest Paid

$450,000

Time in Debt

30 Years

Extra Cost vs Loan +130%

A 6.5% INTEREST RATE DOESN'T MEAN YOU PAY 6.5%... IT CAN MEAN PAYING OVER 100% OF THE LOAN AMOUNT IN INTEREST

THE RATE TELLS YOU HOW THE LOAN IS PRICED...

THE TOTAL INTEREST PAID TELLS YOU WHAT IT ACTUALLY

COSTS

You weren't taught this in school, but...

The Traditional Mortgage Path Is More Expensive Than Most People Realize

Going By The Numbers (national averages)

WHAT MOST PEOPLE LOOK AT

Home Price

$400,000

Loan Amount

$350,000

Interest Rate

6.5%

Monthly Payment

~$2,200

WHAT YOU SEE...

WHAT YOU ACTALLY PAY

WHAT IT ACTUALLY COSTS

Total Paid to Bank

$800,000

Total Interest Paid

$450,000

Time in Debt

30 Years

Extra Cost vs Loan

+130%+

A 6.5% INTEREST RATE DOESN'T MEAN YOU PAY 6.5%... IT CAN MEAN PAYING OVER 100% OF THE LOAN AMOUNT IN INTEREST

THE RATE TELLS YOU HOW THE LOAN IS PRICED...

THE TOTAL INTEREST PAID TELLS YOU WHAT IT ACTUALLY

COSTS

What Would It Mean If Your Home Was Paid Off In 10 Years Instead Of 30...

WITHOUT

Sacrificing your current lifestyle

(no living on rice & beans or giving up the things you enjoy just to get ahead)

Making extra payments

(No double or extra payments - continue making the minimum)

Your money disappearing to the bank along the way

(Instead of losing hundreds of thousands in interest, your dollars are positioned for your perpetual benefit)

WHILE

Improving cash flow efficiency

(structured to do more than one job at the same time - instead of being locked into a single use)

Reducing how much interest you actually pay

(focused on minimizing total interest over time - not just chasing the lowest rate)

Building accessible capital along the way

(creating financial flexibility instead of locking your money away behind fees, penalties, & tax burdens)

That’s The Difference in Outcome When You Meet With a Forever Debt Free Mortgage Loan Officer

Most mortgage professionals are trained to focus on one thing:

securing the lowest possible interest rate.

But as you’ve seen, the rate alone doesn’t determine the outcome—

the strategy & structuring determines how much you actually pay over time.

That’s why our partner loan officers approach things differently.

Instead of focusing only on short-term approval and monthly payment,

they’re trained to help you structure your mortgage in a way that prioritizes long-term efficiency, reduced interest, and greater financial control.

Before you lock into a 30-year obligation… it’s worth seeing what your options actually look like.

What Would It Mean If Your Home Was Paid Off In 10 Years Instead Of 30...

WITHOUT

Sacrificing your current lifestyle

(no living on rice & beans or giving up the things you enjoy just to get ahead)

Making extra payments

(No double or extra payments - continue making the minimum)

Your money disappearing to the bank along the way

(Instead of losing hundreds of thousands in interest, your dollars are positioned for your perpetual benefit)

WHILE

Improving cash flow efficiency

(structured to do more than one job at the same time - instead of being locked into a single use)

Reducing how much interest you actually pay

(focused on minimizing total interest over time - not just chasing the lowest rate)

Building accessible capital along the way

(creating financial flexibility instead of locking your money away behind fees, penalties, & tax burdens)

That’s The Difference in Outcome When You Meet With a Forever Debt Free Mortgage Loan Officer

Most mortgage professionals are trained to focus on one thing:

securing the lowest possible interest rate.

But as you’ve seen, the rate alone doesn’t determine the outcome—

the strategy & structuring determines how much you actually pay over time.

That’s why our partner loan officers approach things differently.

Instead of focusing only on short-term approval and monthly payment,

they’re trained to help you structure your mortgage in a way that prioritizes long-term efficiency, reduced interest, and greater financial control.

Before you lock into a 30-year obligation… it’s worth seeing what your options actually look like.

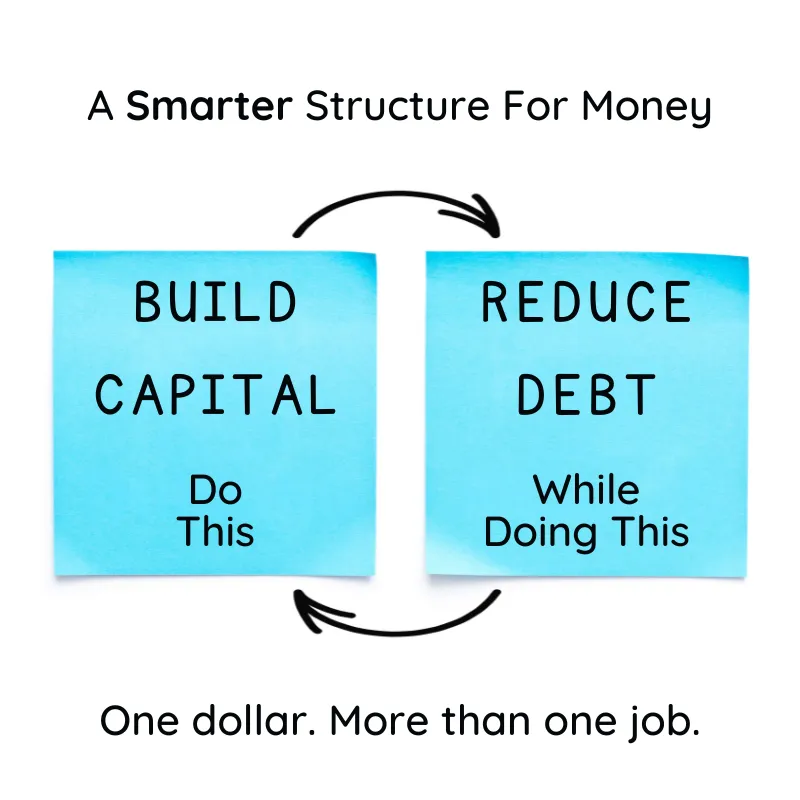

Here's Why You Should Talk With A Forever Debt Free Mortgage Advisor

The Difference Isn't the Loan... It's How the Money is Structured

Most financial decisions force money into a single role at a time.

It either goes toward paying down debt…

or it sits in savings…

or it’s set aside for the future.

But rarely all at once.

With the right structure, your money doesn’t have to choose.

The same dollars can be positioned to work in more than one place at the same time...

helping you reduce debt while still building accessible capital along the way.

And when that happens, the entire outcome changes.

Here's Why You Should Talk With A Forever Debt Free Mortgage Advisor

The Difference Isn't the Loan... It's How the Money is Structured

Most financial decisions force money into a single role at a time.

It either goes toward paying down debt…

or it sits in savings…

or it’s set aside for the future.

But rarely all at once.

With the right structure, your money doesn’t have to choose.

The same dollars can be positioned to work in more than one place at the same time...

helping you reduce debt while still building accessible capital along the way.

And when that happens, the entire outcome changes.

The Questions Smart Homebuyers Are Asking Today

Buying a home is one of the biggest financial decisions most people ever make. These are some of the most common questions we help people think through before choosing a mortgage strategy.

Should I pay off debt before buying a house?

Not necessarily.

In many cases, the better question is whether your overall cash flow is structured efficiently.

Some types of debt may affect what you qualify for, while other situations can be managed strategically without delaying homeownership for years.

The key is understanding how a mortgage fits into your bigger financial picture — not just eliminating debt blindly before buying.

How much house can I realistically afford?

What a bank approves you for and what feels financially comfortable long-term are often two very different numbers.

A healthy mortgage strategy should leave room for:

• savings

• emergencies

• lifestyle flexibility

• future goals

The right number isn’t just about qualifying — it’s about sustainability and financial breathing room.

What should I know before getting pre-approved?

Pre-approval is more than just a rate quote. It’s one of the first opportunities to structure your mortgage intentionally.

Many buyers focus only on:

• interest rate

• monthly payment

• down payment

But factors like loan structure, cash flow, debt load, and long-term payoff strategy can have a major impact over time.

Asking the right questions early can make a significant difference later.

How important is my interest rate compared to my overall mortgage strategy?

Interest rate matters — but it’s only one piece of the puzzle.

Two homeowners can have similar rates and completely different financial outcomes depending on:

• how their cash flow is structured

• how quickly they reduce debt

• how much liquidity they maintain

• how efficiently they use their money over time

Sometimes the “best” mortgage isn’t simply the one with the lowest rate.

What’s the smartest way to pay off a mortgage early?

There’s more than one way to pay off a house early.

Some strategies focus on making larger mortgage payments, while others focus on improving overall cash flow and using money more efficiently across your financial system.

The best approach often depends on:

• income stability

• debt structure

• savings habits

• long-term goals

That’s why personalization matters.

Can I pay off my home faster without increasing my monthly budget?

In many cases, yes.

Many homeowners are surprised to learn that improving the efficiency of existing cash flow can often create opportunities to accelerate debt payoff without simply “spending more.”

The strategy matters just as much as the amount.

Is it possible to build savings while paying off debt?

Yes. That's a feature baked into the structuring and strategies offered by every Forever Debt Free Mortgage Loan Officer.

One of the biggest financial frustrations people experience is feeling like they have to choose between:

• making financial progress

• or maintaining liquidity

We help people structure their loans with a strategy designed to improve both at the same time.

Will paying off my mortgage early hurt my ability to build wealth?

Not always — but how you approach it matters.

Some payoff strategies prioritize eliminating debt as quickly as possible, even if it leaves little flexibility or accessible capital along the way.

Others aim to balance:

• debt reduction

• liquidity

• long-term financial growth

The right balance depends on your goals and financial priorities.

Why does it feel like my mortgage balance barely goes down at first?

What you're feeling is a mechanism most traditional mortgages use called amortization, which means a much larger portion of your early payments goes toward interest rather than principal.

In other words, much of the interest is effectively paid back to the lender during the first half of the loan, while the actual balance often decreases much more slowly than many homeowners expect.

Then, around the time the payment schedule finally starts shifting more heavily toward principal reduction, many borrowers begin receiving offers to refinance — which can restart the amortization cycle all over again.

That doesn’t automatically mean refinancing is bad, but it does mean understanding how mortgage structure works can have a major impact on your long-term financial outcome.

Why do some homeowners still feel financially stressed even with a low interest rate?

Because interest rate alone doesn’t determine financial flexibility.

Cash flow, debt structure, savings habits, and unexpected expenses all play a role in how “comfortable” a mortgage actually feels month to month.

A lower rate can help — but it doesn’t automatically create a stronger financial foundation.

What happens during the virtual strategy session?

The session is designed to help you better understand your current situation and explore what options may be available based on your goals.

We’ll typically review things like:

• mortgage structure

• debt

• cash flow

• financial priorities

• long-term objectives

The goal is education and clarity — not pressure. Every household is different, which is why strategy matters.

The Questions Smart Homebuyers Are Asking Right Now

Buying a home is one of the biggest financial decisions most people ever make. These are some of the most common questions we help people think through before choosing a mortgage strategy.

Should I pay off debt before buying a house?

Not necessarily.

In many cases, the better question is whether your overall cash flow is structured efficiently.

Some types of debt may affect what you qualify for, while other situations can be managed strategically without delaying homeownership for years.

The key is understanding how a mortgage fits into your bigger financial picture — not just eliminating debt blindly before buying.

How much house can I realistically afford?

What a bank approves you for and what feels financially comfortable long-term are often two very different numbers.

A healthy mortgage strategy should leave room for:

• savings

• emergencies

• lifestyle flexibility

• future goals

The right number isn’t just about qualifying — it’s about sustainability and financial breathing room.

What should I know before getting pre-approved?

Pre-approval is more than just a rate quote. It’s one of the first opportunities to structure your mortgage intentionally.

Many buyers focus only on:

• interest rate

• monthly payment

• down payment

But factors like loan structure, cash flow, debt load, and long-term payoff strategy can have a major impact over time.

Asking the right questions early can make a significant difference later.

How important is my interest rate compared to my overall mortgage strategy?

Interest rate matters — but it’s only one piece of the puzzle.

Two homeowners can have similar rates and completely different financial outcomes depending on:

• how their cash flow is structured

• how quickly they reduce debt

• how much liquidity they maintain

• how efficiently they use their money over time

Sometimes the “best” mortgage isn’t simply the one with the lowest rate.

What’s the smartest way to pay off a mortgage early?

There’s more than one way to pay off a house early.

Some strategies focus on making larger mortgage payments, while others focus on improving overall cash flow and using money more efficiently across your financial system.

The best approach often depends on:

• income stability

• debt structure

• savings habits

• long-term goals

That’s why personalization matters.

Can I pay off my home faster without increasing my monthly budget?

In many cases, yes.

Many homeowners are surprised to learn that improving the efficiency of existing cash flow can often create opportunities to accelerate debt payoff without simply “spending more.”

The strategy matters just as much as the amount.

Is it possible to build savings while paying off debt?

Yes. That's a feature baked into the structuring and strategies offered by every Forever Debt Free Mortgage Loan Officer.

One of the biggest financial frustrations people experience is feeling like they have to choose between:

• making financial progress

• or maintaining liquidity

We help people structure their loans with a strategy designed to improve both at the same time.

Will paying off my mortgage early hurt my ability to build wealth?

Not always — but how you approach it matters.

Some payoff strategies prioritize eliminating debt as quickly as possible, even if it leaves little flexibility or accessible capital along the way.

Others aim to balance:

• debt reduction

• liquidity

• long-term financial growth

The right balance depends on your goals and financial priorities.

Why does it feel like my mortgage balance barely goes down at first?

What you're feeling is a mechanism most traditional mortgages use called amortization, which means a much larger portion of your early payments goes toward interest rather than principal.

In other words, much of the interest is effectively paid back to the lender during the first half of the loan, while the actual balance often decreases much more slowly than many homeowners expect.

Then, around the time the payment schedule finally starts shifting more heavily toward principal reduction, many borrowers begin receiving offers to refinance — which can restart the amortization cycle all over again.

That doesn’t automatically mean refinancing is bad, but it does mean understanding how mortgage structure works can have a major impact on your long-term financial outcome.

Why do some homeowners still feel financially stressed even with a low interest rate?

Because interest rate alone doesn’t determine financial flexibility.

Cash flow, debt structure, savings habits, and unexpected expenses all play a role in how “comfortable” a mortgage actually feels month to month.

A lower rate can help — but it doesn’t automatically create a stronger financial foundation.

What happens during the virtual strategy session?

The session is designed to help you better understand your current situation and explore what options may be available based on your goals.

We’ll typically review things like:

• mortgage structure

• debt

• cash flow

• financial priorities

• long-term objectives

The goal is education and clarity — not pressure. Every household is different, which is why strategy matters.